The adverse feedback loop (higher yields=weaker economy =higher default risk=higher yields) remains in full swing in the Eurozone periphery and the dominos are falling one after the other. If nothing changes, then Portugal will have to get a bail-out and after that Spain. With Spain, the capacity of the EFSF would be used up but the capacity of the market to cause more havoc will remain as the focus is likely to shift to Belgium and then Italy. At the latest with a potential bail-out of Spain, something has to happen. What are the options for the Eurozone?

A) Sovereign default: a sovereign default, be it for Greece, Ireland or any other Eurozone member would be disastrous at present. Should any sovereign default on its bond obligations, then the downward spiral would intensify even further and affect even more countries. Furthermore, the banking sectors of the core countries would be affected significantly - amid their holdings of peripheral debts - threatening the core economies. Given the adversity of this scenario, I am convinced that European authorities/politicians will do everything they can to prevent it from happening.

B) Significant quantitative easing by the ECB: As mentioned in my last blog post (Will the real ECB please stand up?), the monetary transmission mechanism in the Eurozone is not working properly. Should the ECB engage in massive quantitative easing (several hundred billions of peripheral bond buying), it could change the dynamics significantly. The ECB bond buying would depress peripheral bond yields sharply and help these sovereigns to continue financing its debt without needing a bail-out. Given such a massive ECB bond buying which breaks the adverse feedback loop, private investors could also move back on the buying side. This could be implemented very easily but the consensus within the ECB for such a course of action is not there (yet).

C) Joint Eurobond issuance. A fairly sensible solution would be to start with joint issuance. A new central agency would issue Eurobonds. Each country could finance up to the criteria set in the stability pact, i.e. up to a maximum outstanding amount of 60% relative to GDP and up to a maximum new issuance each year of 3% of GDP. Any financing needs exceeding these limits would continue to be financed via national bonds (i.e. Bunds, BTPs, BONOs etc.) which, however, would be subordinate to the Eurobonds. Given the much more limited outstanding amounts of the new national bonds, default on these bonds becomes more likely as the risk of contagion and the risk of a systemic financial sector crisis would be much lower. The credit risk and liquidity of these national bonds would be lower and hence yields higher, much higher for the peripheral countries. As a result, the market would continue to differentiate between issuers and hence there would be very strong incentives for each country to remain within the stability pact criteria (much stronger incentives than there were in the past). Additionally, if Eurobond issuance were to start now, the peripheral countries could refinance all their maturing debts and it would take several years before the 60% limit would be reached. The financing via national bonds would be very limited initially (only the part of the deficit exceeding 3%) and could probably be done - at high rates - with short maturity bonds. The implementation, though, seems difficult and there is no political will to engage in such a course of action (yet).

D) A doubling up of the EFSF: this would just prolong the current downward spiral. It would not break the adverse feedback loop (higher yields-weaker economy-higher default risk-higher yields) and the bail-outs would likely continue. However, it would still not be enough to deal with a potential bail-out of Italy. Such a doubling up per se would not offer a lasting solution. Alternatively, a doubling up + ECB buying to a much higher degree where a total of approx. EUR 2trn could be provided would be a different thing as it would guarantee financing and would reduce market rates.

E) A Eurozone break-up. Should the Eurozone break up, the most likely course of action would be for a formation of two separate currency areas (Euro north and Euro south). For a single country to leave, the economic costs would be almost unbearable. A weak country would lose all access to financial markets, could not service its EUR-denominated debts and would need to default. A strong country would see its new currency skyrocket, threatening to kill exports and the banking sector (because they hold a lot of assets denominated in the now weaker EUR). The only half-way realistic scenario would be for the northern block (Germany, Austria, Finland, Netherlands, Luxembourg, potentially Belgium) to form a new currency area which would limit the appreciation effects/reduce the loss of exports/devaluation of banking assets. On the other side a weak country could only leave as a group as well (Greece together with Spain, Portugal, Italy and maybe France) to form a new larger group with a meaningful internal economic and financial market which is still able to attract some foreign capital. However, for such a separation there would need to be a very strong political will (given the super high costs involved) and in turn a democratic legitimation to engage in such a course of action. But for such political movements to form, it needs time, i.e. some years.

Overall, amid the complexity, the costs involved and potential time it needs, a Eurozone break-up remains highly unlikely. Rather, the current path will continue to be taken up until a large country (probably Spain) needs a bail-out and the capacity of the EFSF is being used up. At that stage the political will to start with joint Eurobond issuance or the consensus within the ECB to engage in massive quantitative easing are likely to form, i.e. I think that the most likely scenario is the one of ECB QE (done in conjunction with a topping up in the EFSF), followed by joint Eurobond issuance. Together, I would assign these scenarios a probability of around 60-70%. Up to that point we can continue to watch the dominos fall.

Friday, November 26, 2010

Wednesday, November 17, 2010

Monetary easing in the wrong places or will the real ECB please stand up?

It should have been the ECB and not the US Fed which embarks on another round of quantiative easing.

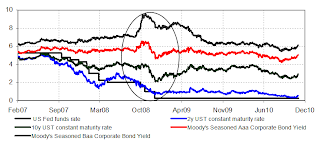

The US Federal Reserve has started their second round of Quantitative Easing which they announced at their last meeting. The first round of QE (and credit easing) was conducted in the wake of the Lehman bankruptcy. At that stage credit yields were rising despite a lower Fed funds rate and lower short-end UST yields (see chart below). These rising yields led to a further worsening of the fundamental situation and increased the risk of corporate bankruptcy which in turn led to higher yields: the negative feedback loop. As a result, the credit/quantitative easing efforts by the US Fed had a significant impact on market pricing and with that on the economy.

Source: Bloomberg, St. Louis Federal Reserve

Source: Bloomberg, St. Louis Federal Reserve

Now, however, neither the level of yields nor the availability of liquidity for the banking sector is holding back the economy. Bond yields have been at historic lows (such as for short-term yields) or at least close (at the longer end). Furthermore, credit-related yields are also at historic low levels, be it in nominal as well as in real terms. Additionally, banks continue to hold a significant amount of excess reserves. In turn, the effect of additional liquidity injection by the US Fed’s Treasury purchases on the real economy in the US should be limited. Rather, the economy is suffering from a lack of aggregate demand which could be eased by additional fiscal spending. But for that the political will is lacking. Overall, despite the additional monetary easing, the outlook for the US economy remains for an extended period of limited growth, but I see only a low risk for a double-dip in the next few quarters. Winter promises to see a slight rebound from the weaker numbers of the last months.

In the Eurozone, however, the ECB is keen to continue its exit from the exceptional liquidity support measures. This is also evident in the rising money-market rates. Several prominent members of the ECB/national Eurozone central banks also feel at unease with the historic low ECB repo rate.

Indeed, the overall Eurozone growth environment with growth at a non-annualised 0.4% in Q3 and yoy inflation currently running around 1.9% (1.1% for the core rate) suggests that it could withstand a somewhat less accommodative monetary policy environment. However, this is not how things work in the Eurozone. The Eurozone is a combination of unequal economies with the outperforming economies enjoying the most accommodative monetary environment and the underperforming economies suffering from the most restrictive monetary environment.

Most notably Germany could do with higher yields. It is one of my long-held believes that Germany is at the start of a multi-year high-growth period. Given that Germany has the lowest nominal bond yields, it has currently also the lowest real yields and in conjunction with a healthy growth environment, it is relatively easy for corporates and households to access credit. As Germany is outperforming, its monetary environment becomes even more accommodative, reinforcing the upswing.

Source: Bloomberg

Source: Bloomberg

On the other side, for example Ireland has much higher nominal yields and given that it suffers from deflation (yoy inflation stood at -0.8% in October), has extremely high real yields. Furthermore, amid the ongoing deep recession, credit is much more difficult to come by for corporates and households. Both, the restrictive credit environment and the highly restrictive level of real yields are reinforcing the deleveraging process and thereby acting to slow down the economy further. This is debt-deflation at its best and results in a downward spiral with the worsening fundamental environment deferring investors, thereby leading to higher yields and with that to ever stronger deleveraging pressures and so on.

For the ECB, this poses indeed a difficult task: The largest economy as well as the Eurozone average would demand a less accommodative environment but the peripheral countries need a more accommodative environment. With the help of their traditional rate setting, they only can lower the level of core bond yields. For the group of peripheral countries where the negative feedback loop is alive, the low repo rate environment has limited effects. If the ECB were up to a more activist stance, it could hike the repo rate but at the same time engage in massive credit (sterilised) or quantitative easing (non-sterilised) via buying of peripheral bonds. With that it would achieve both goals: a somewhat less accommodative environment for the economically sound and well-growing countries but a less restrictive stance for the periphery. Furthermore, the ECB’s support for secondary bond prices would also promote private sector demand for these instruments and limit contagion for other peripheral countries.

So far, the ECB bond buying has been very limited and was thereby not able to break the negative feedback loop. Unfortunately, I only see a low probability that the ECB will seriously step up its bond buying efforts given the prominent adversaries of the existing low-scale buying. Rather it seems likely that we continue facing a re-active ECB which will lead to an even easier monetary environment for the north-east but not the periphery. It should not be the US Fed which is engaging on another round of quantitative easing, it should be the ECB! But as it isn’t, the peripheral countries will continue to suffer from a very restrictive monetary policy environment. For the time being, we can continue to watch the Irish domino fall and once the bail-out has been announced, the focus can shift to Portugal and at a later stage to Spain.

The US Federal Reserve has started their second round of Quantitative Easing which they announced at their last meeting. The first round of QE (and credit easing) was conducted in the wake of the Lehman bankruptcy. At that stage credit yields were rising despite a lower Fed funds rate and lower short-end UST yields (see chart below). These rising yields led to a further worsening of the fundamental situation and increased the risk of corporate bankruptcy which in turn led to higher yields: the negative feedback loop. As a result, the credit/quantitative easing efforts by the US Fed had a significant impact on market pricing and with that on the economy.

US: Negative feedback loop in 2008/09, but not now

Source: Bloomberg, St. Louis Federal Reserve

Source: Bloomberg, St. Louis Federal ReserveNow, however, neither the level of yields nor the availability of liquidity for the banking sector is holding back the economy. Bond yields have been at historic lows (such as for short-term yields) or at least close (at the longer end). Furthermore, credit-related yields are also at historic low levels, be it in nominal as well as in real terms. Additionally, banks continue to hold a significant amount of excess reserves. In turn, the effect of additional liquidity injection by the US Fed’s Treasury purchases on the real economy in the US should be limited. Rather, the economy is suffering from a lack of aggregate demand which could be eased by additional fiscal spending. But for that the political will is lacking. Overall, despite the additional monetary easing, the outlook for the US economy remains for an extended period of limited growth, but I see only a low risk for a double-dip in the next few quarters. Winter promises to see a slight rebound from the weaker numbers of the last months.

In the Eurozone, however, the ECB is keen to continue its exit from the exceptional liquidity support measures. This is also evident in the rising money-market rates. Several prominent members of the ECB/national Eurozone central banks also feel at unease with the historic low ECB repo rate.

Indeed, the overall Eurozone growth environment with growth at a non-annualised 0.4% in Q3 and yoy inflation currently running around 1.9% (1.1% for the core rate) suggests that it could withstand a somewhat less accommodative monetary policy environment. However, this is not how things work in the Eurozone. The Eurozone is a combination of unequal economies with the outperforming economies enjoying the most accommodative monetary environment and the underperforming economies suffering from the most restrictive monetary environment.

Most notably Germany could do with higher yields. It is one of my long-held believes that Germany is at the start of a multi-year high-growth period. Given that Germany has the lowest nominal bond yields, it has currently also the lowest real yields and in conjunction with a healthy growth environment, it is relatively easy for corporates and households to access credit. As Germany is outperforming, its monetary environment becomes even more accommodative, reinforcing the upswing.

Eurozone: Negative fedback loop is still alive (10y yields)

Source: Bloomberg

Source: BloombergFor the ECB, this poses indeed a difficult task: The largest economy as well as the Eurozone average would demand a less accommodative environment but the peripheral countries need a more accommodative environment. With the help of their traditional rate setting, they only can lower the level of core bond yields. For the group of peripheral countries where the negative feedback loop is alive, the low repo rate environment has limited effects. If the ECB were up to a more activist stance, it could hike the repo rate but at the same time engage in massive credit (sterilised) or quantitative easing (non-sterilised) via buying of peripheral bonds. With that it would achieve both goals: a somewhat less accommodative environment for the economically sound and well-growing countries but a less restrictive stance for the periphery. Furthermore, the ECB’s support for secondary bond prices would also promote private sector demand for these instruments and limit contagion for other peripheral countries.

So far, the ECB bond buying has been very limited and was thereby not able to break the negative feedback loop. Unfortunately, I only see a low probability that the ECB will seriously step up its bond buying efforts given the prominent adversaries of the existing low-scale buying. Rather it seems likely that we continue facing a re-active ECB which will lead to an even easier monetary environment for the north-east but not the periphery. It should not be the US Fed which is engaging on another round of quantitative easing, it should be the ECB! But as it isn’t, the peripheral countries will continue to suffer from a very restrictive monetary policy environment. For the time being, we can continue to watch the Irish domino fall and once the bail-out has been announced, the focus can shift to Portugal and at a later stage to Spain.

Wednesday, November 10, 2010

A disintegrating Eurozone?

One disturbing development within the Eurozone is the reduction in internal trade flows as well as the domestication of some debt markets.

This FT article states that "Foreign holdings of Portuguese and Irish bonds fell to 65% of total debt at the end of the second quarter from 85% in 2009. They fell to 55% from 70% in Greece and to 38% from 43% in Spain during the same period." As foreigners stopped buying the bonds of these countries, domestic institutions (mostly banks, but apparently also pension funds and insurance companies) were buying them.

As a result holdings by other countries of these bonds fell. The table below shows the foreign assets of the German banking sector of other Eurozone countries at the end of 2008 as well as in September this year and the %-changes. In combination, German banks reduced their holdings of assets in Greece, Ireland, Portugal and Spain by more than 15% whereas they increased the assets relating to neighbouring Eurozone countries by almost 5%. Furthermore, they also decreased the assets of the other southern European countries, most notably Italy.

As a result holdings by other countries of these bonds fell. The table below shows the foreign assets of the German banking sector of other Eurozone countries at the end of 2008 as well as in September this year and the %-changes. In combination, German banks reduced their holdings of assets in Greece, Ireland, Portugal and Spain by more than 15% whereas they increased the assets relating to neighbouring Eurozone countries by almost 5%. Furthermore, they also decreased the assets of the other southern European countries, most notably Italy.

German banks' foreign assets holdings (in €mln)

| Dec 2008 | Sep 10 | %-change | |

| Belgium | 25.392 | 31.700 | 20% |

| Finland | 8.401 | 8.713 | 4% |

| France | 152.400 | 171.338 | 11% |

| Greece | 28.550 | 29.044 | 2% |

| Ireland | 188.051 | 157.519 | -19% |

| Italy | 144.257 | 115.338 | -25% |

| Luxembourg | 191.005 | 189.383 | -1% |

| Malta | 7.643 | 7.154 | -7% |

| Netherlands | 118.075 | 120.170 | 2% |

| Austria | 76.688 | 78.098 | 2% |

| Portugal | 27.859 | 25.665 | -9% |

| Slowakia | 2.727 | 2.809 | 3% |

| Slovenia | 4.425 | 3.593 | -23% |

| Spain | 176.909 | 149.762 | -18% |

| Cyprus | 8.017 | 7.021 | -14% |

| SP,GR,IR,PO | 421.369 | 361.990 | -16% |

| AT,NL,FR,BE,LU | 563.560 | 590.689 | 5% |

| IT,FI,SL,SL,CY,MA | 175.470 | 144.628 | -21% |

| Total | 1.160.399 | 1.097.307 | -6% |

Source: German Bundesbank

But also in terms of trade flows, a similar picture emerges. The table below shows the German exports and imports from June-Aug 2010 compared to the same period in 2007. Exports to Portugal, Ireland, Greece and Spain decreased by almost one fourth, highlighting the weak state of these economies. However, imports from these countries also dropped by a significant 7%. In contrast, German exports to its neighbouring Eurozone countries (France, Netherlands, Austria, Belgium, Luxembourg) increased slightly by 2% whereas imports from neighoubirng countries increased by a significant 6%. In between is the group of non-SGIP/non-neighbouring Eurozone countries (Italy, Finland, Slovenia, Slovakia, Malta, Cyprus) where Germany saw its exports drop by almost 8% and imports drop by 3%. Interesting is also the development of German trade flows vs. its non-Eurozone neighbours (Poland, Denmark, Czech Republic, Switzerland, Liechtenstein) which have increased significantly vs. 2007.

German imports and exports Jun-Aug 2010 in €bn & %-changes vs. same period 2007

Source: German Statistics Office, Research Ahead

Source: German Statistics Office, Research Ahead

Yes, Germany is exporting its improved business environment via higher imports, but mostly to its neighbouring countries and less to the fiscally challenged SGIP.

Overall, the combination of the changes in cross-border holdings of financial assets as well as in the composition of trade flows suggests that the group of fiscsally challenged countries - Spain, Greec, Ireland, Portugal - is seeing its economic ties with the rest of the Eurozone weaken significantly, i.e. to some degree they have been disintegrating from the rest of the Eurozone. As a result, so far they could not profit that much from the economic rebound in the north-eastern Eurozone countries.

On the other side, the already rather strong economic integration of the north-eastern Eurozone countries is intensifying further.

Should these economic developments run further - disintegration of the fiscally challenged economies from the rest of the Eurozone, intensifying integration of the economically stronger north-eastern countries - political realities could start to mirror these developments via the formation of a north-eastern political club with a weakening of the will for ongoing support measures to the rest of the Eurozone.

Overall, the combination of the changes in cross-border holdings of financial assets as well as in the composition of trade flows suggests that the group of fiscsally challenged countries - Spain, Greec, Ireland, Portugal - is seeing its economic ties with the rest of the Eurozone weaken significantly, i.e. to some degree they have been disintegrating from the rest of the Eurozone. As a result, so far they could not profit that much from the economic rebound in the north-eastern Eurozone countries.

On the other side, the already rather strong economic integration of the north-eastern Eurozone countries is intensifying further.

Should these economic developments run further - disintegration of the fiscally challenged economies from the rest of the Eurozone, intensifying integration of the economically stronger north-eastern countries - political realities could start to mirror these developments via the formation of a north-eastern political club with a weakening of the will for ongoing support measures to the rest of the Eurozone.

Wednesday, November 3, 2010

German Wirtschaftswunder revisited

I have been arguing for a long time that the multi-year outlook for the German economy is extremely positive (see for example There is more to celebrate for Germany from Nov last year or German Wirtschaftswunder 2.0 from May this year). In the meantime, economic data out of Germany has surprised most economists and investors. While growth projections have been revised upwards, I remain convinced that the outlook for the German economy (and thus for German real and financial assets) is by far much more favorable.

There are various reasons why this is the case:

a) German corporates have become extremely competitive over the past decade. During the first years of EMU they had to largely regain competitiveness vs. the rest of the Eurozone as Germany locked in an uncompetitive exchange rate when the euro was formed and German corporates were heavily in financial deficit following the debt-financed M&A boom during the dot-com bubble. In turn, at the start of the last decade German corporates had to restructure (i.e. cut costs - especially via headcount reduction in Germany and offshoring/outsourcing) to regain cost competitiveness and reduce the financial deficit. Unfortunately, as Germany regained internal competitiveness during the last decade, the external value of the euro soared, especially vs. key competititors such as Japan. However, over the past 2 years, the euro has lost altitude - again especially vs. key competitors - and German corporates for the first time since the start of EMU are competitive on an intra-Eurozone and on an extra-Eurozone basis. Additionally, German corporates on aggregate have moved from a financial deficit into a financial surplus.

b) German households have been burdened over the past decade by the restructuring of the corporate sector and the numerous reforms by the state of amongst others the labour market, the unemployment benefits as well as the pension systems. In combination they had the effect of rising the financial risks carried by each individual (via lower job security and lower social security), temporarily increasing unemployment and reducing wage growth. All this put downward pressure on the sum of wages earned and upward pressure on the German savings ratio, in turn creating an environment of weak domestic demand. However, now the sum of wages earned is increasing (as unemployment dropped sharply and we are likely to enter an upcycle in wage growth) while no more significant structural reforms are on the agenda. In turn, the outlook for consumption growth has become favorable as well for the first time since the start of EMU.

c) The Germans state was forced to carry through numerous structural reforms as well as several rounds of fiscal tightening to reduce the structural fiscal deficit. However, at present the situation of German state finances is relatively healthy and in turn the need to carry through fiscal tightening measures is limited. The German government decided to engage on a 4-year tightening programme, but on average the tightening amounts to only approx. 0.25% of GDP per year. Furthermore, as the economy is doing better than anticipated, fiscal deficits are undershooting the projected levels by a significant margin.

d) At the start of EMU, Germany had a high price level which combined with weak economic developments resulted in below-average inflation and thus in above-average real yields, further restraining the economy. Now, however, the German economy is roaring ahead which should lead to inflation being more in-line with the Eurozonea average. Additionally, intra-Eurozone sovereign spreads are very high and as a result, Germany is enjoying the lowest real yields within the Eurozone. Finally, as the outlook for the German economy is favorable, credit conditions are easing. As a result, for the first time since the start of EMU, Germany enjoys a very accommodative monetary environment.

What is more, all of these factors re-inforce each other. While at the beginning of the last decade this lead to a vicious circle whereby weakness in the corporate sector, the household sector, a restrictive fiscal and monetary environment all reinforced each other, we are now just at the beginning of a virtuous circle.

The strength in the corporate sector is leading to more employment and with that wage and consumption growth. The outlook for the domestic economy is thereby improving, leading corporates to invest more and banks to provide more funds (as the perceived credit risk is lowered). The fiscal deficit is reduced which reduces the need for fiscal tightening/opens the door for fiscal easing. Domestic inflation picks up which - given that Germany outperforms the rest of EMU - leads to lower real yields, further promoting more investments and a lower savings ratio. Within the monetary union if a country starts to outperform in economic terms, its monetary environment becomes even more accommodative not less, further reinforcing the upswing.

Given the favorable starting point for Germany in terms of corporate competitiveness and low private sector indebtedness such a virtuous circle can last for years without leading to cost disadvantages and/or over-indebtedness.

We are just at the start of this virtuous circle where the drop in unemployment - due to the export led growth rebound - starts to fuel wage gains and coupled with low real yields promotes a reduction in the savings ratio. This will create an increasingly favorable environment for domestic demand and lead to the next wave in growth. I remain convinced that Germany will show above trend growth for the next 3-5 years. While there will be ups and downs in quarterly growth numbers, I continue to look for growth to average around 2.5-3%.

There are various reasons why this is the case:

a) German corporates have become extremely competitive over the past decade. During the first years of EMU they had to largely regain competitiveness vs. the rest of the Eurozone as Germany locked in an uncompetitive exchange rate when the euro was formed and German corporates were heavily in financial deficit following the debt-financed M&A boom during the dot-com bubble. In turn, at the start of the last decade German corporates had to restructure (i.e. cut costs - especially via headcount reduction in Germany and offshoring/outsourcing) to regain cost competitiveness and reduce the financial deficit. Unfortunately, as Germany regained internal competitiveness during the last decade, the external value of the euro soared, especially vs. key competititors such as Japan. However, over the past 2 years, the euro has lost altitude - again especially vs. key competitors - and German corporates for the first time since the start of EMU are competitive on an intra-Eurozone and on an extra-Eurozone basis. Additionally, German corporates on aggregate have moved from a financial deficit into a financial surplus.

b) German households have been burdened over the past decade by the restructuring of the corporate sector and the numerous reforms by the state of amongst others the labour market, the unemployment benefits as well as the pension systems. In combination they had the effect of rising the financial risks carried by each individual (via lower job security and lower social security), temporarily increasing unemployment and reducing wage growth. All this put downward pressure on the sum of wages earned and upward pressure on the German savings ratio, in turn creating an environment of weak domestic demand. However, now the sum of wages earned is increasing (as unemployment dropped sharply and we are likely to enter an upcycle in wage growth) while no more significant structural reforms are on the agenda. In turn, the outlook for consumption growth has become favorable as well for the first time since the start of EMU.

c) The Germans state was forced to carry through numerous structural reforms as well as several rounds of fiscal tightening to reduce the structural fiscal deficit. However, at present the situation of German state finances is relatively healthy and in turn the need to carry through fiscal tightening measures is limited. The German government decided to engage on a 4-year tightening programme, but on average the tightening amounts to only approx. 0.25% of GDP per year. Furthermore, as the economy is doing better than anticipated, fiscal deficits are undershooting the projected levels by a significant margin.

d) At the start of EMU, Germany had a high price level which combined with weak economic developments resulted in below-average inflation and thus in above-average real yields, further restraining the economy. Now, however, the German economy is roaring ahead which should lead to inflation being more in-line with the Eurozonea average. Additionally, intra-Eurozone sovereign spreads are very high and as a result, Germany is enjoying the lowest real yields within the Eurozone. Finally, as the outlook for the German economy is favorable, credit conditions are easing. As a result, for the first time since the start of EMU, Germany enjoys a very accommodative monetary environment.

What is more, all of these factors re-inforce each other. While at the beginning of the last decade this lead to a vicious circle whereby weakness in the corporate sector, the household sector, a restrictive fiscal and monetary environment all reinforced each other, we are now just at the beginning of a virtuous circle.

The strength in the corporate sector is leading to more employment and with that wage and consumption growth. The outlook for the domestic economy is thereby improving, leading corporates to invest more and banks to provide more funds (as the perceived credit risk is lowered). The fiscal deficit is reduced which reduces the need for fiscal tightening/opens the door for fiscal easing. Domestic inflation picks up which - given that Germany outperforms the rest of EMU - leads to lower real yields, further promoting more investments and a lower savings ratio. Within the monetary union if a country starts to outperform in economic terms, its monetary environment becomes even more accommodative not less, further reinforcing the upswing.

Given the favorable starting point for Germany in terms of corporate competitiveness and low private sector indebtedness such a virtuous circle can last for years without leading to cost disadvantages and/or over-indebtedness.

We are just at the start of this virtuous circle where the drop in unemployment - due to the export led growth rebound - starts to fuel wage gains and coupled with low real yields promotes a reduction in the savings ratio. This will create an increasingly favorable environment for domestic demand and lead to the next wave in growth. I remain convinced that Germany will show above trend growth for the next 3-5 years. While there will be ups and downs in quarterly growth numbers, I continue to look for growth to average around 2.5-3%.

Subscribe to:

Comments (Atom)